Before the Noise Comes Back, Read This

You can keep scrolling — or you can slow down and actually understand what you’re holding.

Sometimes crypto feels like being in a giant, chaotic airport.

Everyone’s rushing somewhere, yelling about the terminal they think leads to the moon. Half the signs are fake. The flight times keep changing. And the only people making real progress are the ones who already know where they’re going.

You don’t need to catch every new trend.

But you do need to understand the tools that stick around — and the ones that shaping how things work behind the scenes.

That’s what this week’s about.

AIOZ is one of them.

They’re building decentralized storage, video streaming, and AI compute. Not a whitepaper, not a vision — actual working products. If DePIN becomes real, it’ll be because of projects like this.

APR vs. APY still trips people up.

It’s one of those things you think you get until the numbers don’t add up. We’ll make it simple — and show how these terms shape what people think they’re earning.

Privacy coins aren’t going away.

They don’t get much airtime anymore, but they still solve real problems. This week’s Deep Dive breaks down how they work, what makes them useful, and why they’re under pressure.

Wallet Guard is a quick fix worth doing.

It flags scammy signatures before you click. Nothing fancy. Just one of those tools that saves you when you’re tired, distracted, or moving too fast.

TokenFi is building in the background.

They’re not promising to tokenize the world — they’re just doing it. Real toolkit, live platform, small but active use. It’s worth knowing they exist.

This isn’t an issue full of headlines. (again 😅)

It’s one of those weeks where you get a little sharper, a little more prepared, and maybe notice something others won’t until it’s obvious. That's the whole point of what I am trying to do here.

Let’s get into it.

📸Spotlight Project

— AIOZ Network (AIOZ) —

The Problem No One Thinks About (Until It Breaks)

Most people don’t spend time thinking about how the internet works. We upload photos, stream videos, play with AI tools, and assume it’ll all just… work. Behind the scenes, it’s mostly powered by a few centralized giants—Amazon Web Services, Google Cloud, YouTube, etc.

It’s fast, but also fragile. A single data center going down can disrupt half the world. Storage costs are high. AI models are trapped behind corporate APIs. And your data? Not really yours.

AIOZ Network is trying to fix this—not by replacing one giant with another, but by spreading the infrastructure across regular users and devices, piece by piece. It’s not loud. But if they pull it off, it could reshape how the internet operates.

What AIOZ Is Actually Building

AIOZ isn’t “a streaming coin” or “an AI play.” It’s an infrastructure stack—designed to support the internet’s three biggest needs:

Storage

Streaming

AI computation

Each one is built on a decentralized physical infrastructure network (DePIN), which means regular people can contribute their spare storage, bandwidth, and processing power. They get rewarded in AIOZ tokens. The whole thing runs on a blockchain that combines Ethereum compatibility (so devs don’t have to learn new tools) with Cosmos scalability (so it can actually handle large-scale traffic).

And they’ve already launched real tools.

Decentralized Storage That Doesn’t Feel Like a Downgrade

Most “decentralized storage” platforms feel like a step backward. They’re clunky, slow, or impossible to integrate into normal workflows. AIOZ took a different approach:

S3-compatible: Developers used to AWS can plug in with minimal changes.

Built-in CDN: Content loads faster, globally. No need to pay for separate content delivery networks.

Encryption and privacy: Your data stays encrypted, and AIOZ claims even they can’t access it.

No single point of failure: If one node goes offline, others fill the gap.

This setup is already usable by dApps, websites, or companies that want to reduce cloud costs or gain more control over their data. And because it’s decentralized, there’s no central authority to dictate terms or pricing.

🔧 Fixing IPFS for Real-World Use

AIOZ also offers AIOZ PIN—their improved version of IPFS (Inter Planetary File System) pinning. If you’ve ever seen NFT images disappear or had files go missing on IPFS, you know why this matters.

IPFS works in theory, but in practice, it struggles with persistence and speed. AIOZ PIN fixes that by offering:

Reliable pinning (your files stay online even if your node goes offline)

Faster access via global CDN

Dedicated gateways for uptime and performance

Tools for managing NFT assets, metadata, and large collections

SDKs and APIs that don’t make you want to scream

It’s especially useful for NFT marketplaces, games, and metaverse platforms that need stable file hosting without relying on traditional servers.

AI on the Edge: Local, Private, and Decentralized

Most AI platforms today collect your data, send it to their servers, process it, and return an answer. You get a result, but you give up control. AIOZ takes the opposite approach.

They run AI tasks on local nodes, meaning your data doesn’t need to leave your device or network. That improves:

Privacy: Nothing gets sent to some unknown server

Latency: No waiting for round trips

Efficiency: Uses spare compute from contributors

They’re even building a marketplace for AI models and datasets, so developers and researchers can buy, sell, or license AI tools peer-to-peer—governed by smart contracts and verified by community feedback. If it works, it would open up AI access in a way that’s more equitable and secure than today’s closed platforms.

📡 Streaming Infrastructure Without the Platform Tax

Video is one of the most expensive things to host and deliver. AIOZ makes that cheaper and more flexible.

Their streaming service supports:

Hosting and transcoding (converting videos into playable formats)

Analytics

Standard protocols like HLS and DASH (so it works with existing devices)

Integration via APIs and SDKs

But the real difference is that it’s not a video platform—it’s infrastructure. You’re not joining another YouTube or Twitch clone. You’re building on a decentralized network that handles the heavy lifting, without taking a huge revenue cut or locking you into a platform’s policies.

It’s made for platforms, educators, live event organizers, and even gaming and enterprise teams who want to own the pipeline without building it from scratch.

Is It Worth Watching?

Yes—but not for hype. For fundamentals.

The markets they’re targeting are huge:

Cloud storage: ~$800B

AI infrastructure: ~$2T

Streaming: ~$400B

Even a small piece of those could justify serious value. And since the network is still relatively early, it hasn’t been flooded with speculation or inflated promises.

Here’s how to keep track:

See how their native dApps perform

Watch for new partnerships or use cases

Follow node growth and network activity

Track developer adoption, not just price movement

If you’re in this space for short-term flips, AIOZ probably won’t excite you right now. But if you’re paying attention to long-term infrastructure plays that might quietly power the next wave of Web3… this one’s worth your radar.

⛓️Crypto Basics

— APR vs. APY - Same Percentages, Completely Different Outcomes —

There’s a quiet trick in the way crypto platforms — and even banks — present numbers.

They throw percentages at you like candy:

“Earn 12%!”

“Borrow at just 9%!”

But unless you know whether that number is APR or APY, you don’t actually know what it means.

So let’s stop pretending it’s some advanced finance thing. This is simple. The difference between APR and APY is just compounding — nothing more.

But that one detail changes everything.

🔧 Let’s strip it down.

APR (Annual Percentage Rate) is the flat interest rate. It doesn’t include any growth on top of growth.

APY (Annual Percentage Yield) includes compounding — meaning your gains are reinvested automatically and start generating their own returns.

Here’s how that plays out:

If you lend $1,000 at 10% APR, after one year, you’ll have $1,100.

If you stake $1,000 at 10% APY (compounded monthly), you’ll have about $1,104.71.

That’s a $4.71 difference on a small amount, with just monthly compounding. It doesn’t sound huge — until you scale it up.

Make it $10,000, and you’re looking at nearly $50 difference.

Compound daily or every 8 hours like some crypto protocols do, and the gap gets wider.

Stretch it over multiple years, and it snowballs.

So the key point here is:

APY tells the whole story. APR doesn’t.

🤨 Why they show you one or the other

If a platform wants to make a return look good, they’ll show APY.

If they want to make a cost look small, they’ll show APR.

Same base rate. Different story.

It’s not about deception. It’s about framing. APY inflates the number by including compounding. APR keeps it plain. And if you don’t realize which one you’re looking at, you’ll either:

Overestimate your earnings

Or underestimate what you’ll owe

Both are easy to avoid once you know what to look for.

📊 Real talk about staking

In crypto, you’ll see APY used a lot in staking and yield farming. Sometimes you’ll see 30%, 50%, even triple-digit APYs. Tempting, right?

But here’s the part that gets glossed over:

That APY is usually paid in tokens. If the token drops in value, your return gets wrecked — even if the APY number looks great.

Not all APYs are actually compounding. Some platforms pay rewards out daily or weekly, but you have to manually claim and restake. If you don’t do that, the actual return is closer to APR than APY. It only compounds if you take action.

Compounding frequency changes everything. Daily is better than weekly. Hourly is better than daily. Some protocols compound every 8 hours. Some don’t compound at all unless you do it yourself. The more often it compounds, the higher the real APY — even at the same base rate.

So the next time you see something like “Earn 70% APY!” — slow down.

Ask:

How often is it compounded?

Is it automatic?

What token is the reward in?

Is that token even holding its value?

A high APY with a collapsing token or no auto-compounding isn’t a real 70%. It’s just a headline.

APR and loans: where it quietly costs you

APR is mostly used when you’re borrowing — crypto loans, margin, credit cards. It shows you the base cost of the loan, but not how often it’s applied.

If you borrow $1,000 at 12% APR, it sounds like you’ll owe $120 in a year.

But if the platform compounds your balance monthly — meaning they charge interest on the growing amount — you’ll owe more than that. Quietly. Over time.

APR doesn’t tell you that part. You need to look deeper — into whether interest accrues daily, monthly, or otherwise.

Same with fees. APR might not include them. So your real cost could be 14% or 15%, even though the label says 12%.

In crypto-backed loans, this gets especially important. Say you take out a loan at 8% APR using your ETH as collateral. If that loan compounds daily, and you let it ride for a few months — your balance owed will creep up faster than you think.

So again — APR is useful. But it’s not the full picture.

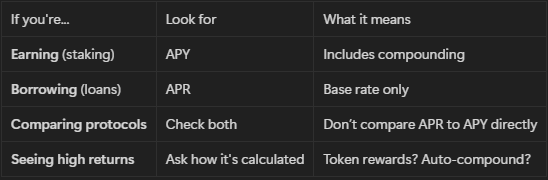

🔩How to actually use this

Here’s the cheat sheet:

💡And one more thing:

If two platforms offer the same base rate, the one using APY is offering more — assuming they’re both actually compounding.

If they’re not, it’s just APR in disguise.

Final takeaway

APR and APY aren’t complicated.

APY includes compounding. APR doesn’t.

But the impact can be huge over time — especially in crypto, where things move fast and change often.

If you’re not sure which one you’re looking at, ask.

If the numbers seem too high, double-check how they’re calculated.

If you’re investing — APY is your guide.

If you’re borrowing — APR is your warning.

And if it still doesn’t make sense, just ask one more question:

"How often does this compound?"

That one question will tell you more than the label ever will.

🔎Deep Dive

— Privacy Coins — What They Are, Why They Matter, and Why They’re Under Fire —

Let’s just say it plainly:

Most people don’t understand privacy coins. And the people who do understand them? A lot of them are trying to make sure you never use them.

They’re treated like a problem. A threat.

But they’re not. They’re just digital cash. That’s really all it is.

You know how when you take cash out of an ATM, your bank knows you took it — but after that, it’s off the grid? You can spend it, give it to someone, burn it, whatever. That part isn’t tracked.

Privacy coins work the same way.

You can get them through an exchange — which is usually recorded. But once they’re in your wallet and you spend them, the transaction details aren’t visible. Nobody else sees who sent what to whom. The chain doesn’t follow you like a shadow.

And in a world where nearly every digital action is monitored, recorded, and mined for value…

that’s actually kind of rare.

⚙️ How They Work (Without Getting Too Technical)

Different privacy coins use different tools to stay private. The tech itself is complicated — zero-knowledge proofs, ring signatures, stealth addresses — but the effect is pretty easy to understand.

Monero (XMR)

When you send Monero, your transaction gets bundled with other transactions that look exactly like yours. So it’s not clear who actually sent what. It also uses stealth addresses, meaning the wallet someone receives funds to isn’t publicly tied to them. Everything is obscured by default.

Zcash (ZEC)

Zcash gives you a choice between transparent or shielded transactions. Shielded ones use zero-knowledge proofs — a method where you prove a valid transaction happened, without showing the actual details. The result? A transaction that’s verifiable but private.

Dash

Dash isn’t a full privacy coin. It offers a feature called PrivateSend, which lets you mix your funds with other users to make it harder to track where the money came from.

There are others, but those are the ones that come up most often.

What’s the Point?

A lot of people ask this:

Why would you need that much privacy unless you’re hiding something?

Here’s the answer:

because you should get to decide who sees your finances.

Most people aren’t doing anything wrong. They just don’t want every crypto payment to be stored in a permanent public history. Or they don’t want advertisers to build another layer to their profile. Or they’re donating to a cause that could get them flagged somewhere. Or maybe they just want the basic dignity of not being watched.

Privacy isn’t about having something to hide.

It’s about having control over what’s yours.

That includes your money.

🏦 Why Governments Are Trying to Ban Them

In the EU, there’s a regulation on the table (called AMLR) that’s trying to make privacy coins — and even anonymous wallets — illegal by 2027.

The reasoning is familiar: terrorism, money laundering, dark web, etc.

But that logic could’ve been used to ban cash decades ago. Some people use it for bad things — yes. But the existence of some bad use doesn’t erase all the good ones. You don’t ban envelopes just because criminals also use envelopes.

This law goes even further than exchanges. It could reach self-custodial wallets. Meaning:

If you own Monero, and someone sends you Monero, and you’re in the EU — you could technically be violating the law. Even if it was a peer-to-peer payment. No middleman involved. Just two people.

That’s not just a crackdown on crypto. That’s a crackdown on financial autonomy.

And the people proposing this often don’t understand how the tech even works. They treat everything anonymous as criminal by default. They’re trying to solve a hard problem with a blunt instrument. And it’s already pushing privacy tools underground.

🟢 Real Use Cases That Don’t Get Talked About

Most people will never use privacy coins to fund something sketchy. But here are a few very normal, very real reasons people use them:

A journalist in a hostile country uses Monero to receive donations without putting their safety at risk.

A business wants to pay a contractor without revealing every other wallet they’ve ever interacted with.

A donor gives to a political cause anonymously, because they don’t want that on a public ledger.

An activist needs to move money without getting flagged or frozen.

Someone just wants to keep their financial life personal, the same way they don’t share every receipt from the grocery store.

These are people who have nothing to hide — they just don’t want to live under constant observation. And if a government wants to know all of these, is it really a modern democratic government?

If You’re Thinking of Using or Investing in Them

You should know the risks. This isn’t investment advice, just some context:

Regulation is the biggest threat. If a coin gets delisted from major exchanges, it becomes harder to buy and sell. That affects liquidity and price.

Some wallets don’t support full privacy features. For example, not all exchanges or wallets allow shielded Zcash transactions. You’ll need to do your homework.

Privacy coins are often harder to use. Monero, for instance, isn’t always easy to buy, depending on where you live.

But the upside is clear too:

There’s growing demand for private, censorship-resistant money. And privacy coins are some of the only working tools that offer that. No theory. No roadmap. They already work.

That’s worth knowing — even if you never buy them.

My Thought

You don’t have to be all-in on privacy coins.

But you should understand why they exist — and why they’re being targeted.

This isn’t about “crypto bros” or tech utopias. It’s all bout whether people should be allowed to transact without reporting their every move to someone else.

If we give that up, even quietly, it’s going to be very hard to get it back. Mark my words…

💰Quick Win of the Week

— Wallet Guard - Quiet Protection for Loud Mistakes —

Most people don’t realize how easy it is to lose everything in crypto.

Not in a dramatic “I got hacked” kind of way.

In the quiet, boring, two-click mistake kind of way.

Click link.

Connect wallet.

Approve signature.

Done. Your NFTs are listed to a scammer for pennies. Or worse — you’ve just given a malicious contract permission to drain everything in your wallet.

And unless you’re reading hex code in real-time, there’s no clear warning. No one yells “stop.” You just learn the hard way.

That’s where Wallet Guard gets handy.

It’s a free browser extension that helps prevent this kind of stuff. It doesn’t replace your wallet. It doesn’t ask for access. It just pays attention — when most people don’t.

What it actually does:

Checks the site you’re visiting.

It notices when a site is new, low-trust, or pretending to be something it’s not. If a link gets shared in a Discord and the site was created 2 days ago? Wallet Guard throws up a warning.

Simulates transactions before you sign them.

It doesn’t just show you gas fees. It shows you what’s about to happen.

“You’re giving permission for this contract to transfer your assets.”

“This signature would list your NFTs on OpenSea.”

That kind of thing. In plain language.

Catches fake stuff early.

Some scams look official. Some even put fake “Secured by Wallet Guard” banners on the site. Doesn’t matter. Wallet Guard catches it before you even connect your wallet.

Lets you ask questions, anytime.

There’s a built-in AI you can use to ask things like “what does this contract do?” or “what’s token approval?”

No account needed. No learning curve. Just straight answers while you’re on the site.

A few things I like about it:

It doesn’t need you to connect your wallet to work.

It doesn’t touch your funds. You don’t even sign anything.

It’s open-source.

You can go on GitHub and read the code. They’re not hiding what it does.

It actually helps new users.

It’s not just for people who already know what they’re doing. It explains things in a way that makes sense. No jargon.

It’s not tied to one chain or one wallet.

Works across Ethereum, Polygon, Arbitrum. Works with Metamask, Trust Wallet, Phantom, etc.

You don’t need to overthink this.

It’s free. It runs in the background. You won’t even notice it — unless it stops you from making a mistake. And that one moment could save you a lot.

I’ve seen it flag legit-looking links that turned out to be scams. I’ve seen it explain complex signatures in one sentence. That kind of quiet support is rare in this space.

If you're the kind of person who’s curious, cautious, or just tired of double-checking everything manually — try it.

Install it once. Let it do its thing.

That’s the win.

PS: This is not an affiliate ad or sponsored content.

💎Small-Cap Gems

— TokenFi (TOKEN) —

TokenFi is one of those projects that makes more sense the longer you sit with it. On the surface, it looks like another tool from meme coin land. And technically, it is — it came out of the Floki ecosystem. But if you get past that and actually look at what they’re building, it’s surprisingly solid.

Here’s the simple version:

TokenFi is a platform for launching tokens and tokenizing real-world assets (RWAs). Think real estate, gold, stocks, collectibles — broken into digital chunks that you can buy, sell, or hold just like any crypto token. They’re trying to make this process so simple that anyone can do it without coding, legal expertise, or jumping through hoops.

And here’s what they already have:

A one-click token launcher

A Telegram bot that lets you launch from your phone

An AI-powered contract auditor

A Launchpad

Tools for RWA tokenization

A DAO system that actually gets used

The tools are live. The token ($TOKEN) powers all of it.

📊Why it matters now

Tokenization isn’t new. People have been talking about it for years. The difference is, traditional finance is finally starting to move. We’re seeing governments (UAE, Singapore, Hong Kong) put actual frameworks in place. BlackRock and JP Morgan are piloting tokenized bonds and stocks. HSBC launched tokenized gold. The institutional side is coming, not in theory — in practice.

That’s where TokenFi fits in. They’re not chasing retail hype right now. They’re building tools that could actually be useful to smaller firms, startups, or even institutions that don’t want to build from scratch. And because it’s crypto-native, it already fits into existing on-chain infrastructure. 24/7 markets. Fractional ownership. No middlemen.

They’re not inventing the trend — they’re just making it easier to access.

What makes it different

TokenFi isn’t a solo bet on one feature. It’s more like a toolbox. You can launch a meme coin. You can tokenize an office building. You can fractionalize a watch or a plot of land. And you can do it without asking a developer for help.

This is the kind of boring infrastructure that becomes useful if the space actually scales.

Also, it’s worth noting:

The Floki community gives them an actual user base. It’s not huge, but it’s real.

The DAO just voted to remove the transaction tax. That helps small users and makes the platform more attractive.

They’ve already supported a ton of smaller token launches — so this isn’t their first cycle.

❗But you need to know the risks

TokenFi has a working product, but the market is still forming. Some risks are obvious:

Regulation. It’s getting better, but it’s not stable yet — especially in the U.S.

Liquidity. This is a small-cap. A few whales moving in or out can swing the price.

Execution. Building is one thing. Growing adoption is another.

Perception. Meme coin roots might turn off some institutional players.

You shouldn’t treat this as some secret alpha. But if you’re building a long-term portfolio that includes asymmetric bets — this one’s worth watching.

The bottom line

TokenFi is trying to do something useful. That alone sets it apart from most low-cap projects. The tools are live. The space it’s targeting is real. And the team seems to be moving steadily rather than hyping the hell out of it.

If tokenized assets become normal in the next few years — and there’s a lot of signs they will — projects like this could become the backbone of how it’s done.

Still early. Still risky. But not noise.

📌 Before You Go…

We talk a lot about cycles. Market cycles. Narrative cycles. Token trends coming and going like fashion. But one thing that doesn’t cycle? Good decision-making.

Most people try to trade the market. Time it. Outrun it. But the more you zoom out, the more it becomes clear: the people who consistently win are the ones who outlast it.

That means asking better questions.

Is this project solving a real problem?

Is anyone actually using it?

Does the team adapt or just post vibes?

And maybe most importantly:

are people still paying attention when prices are down?

Because when the charts are quiet and X is bored, that’s when the best setups start to form. Not just technically—but mentally.

If you're only in this game to catch the next 20x, you're always going to be chasing. But if you're here to understand what makes those 20x stories possible in the first place, you're already ahead of most. That's the way making 20x gains, by securing 2x-3x gains with better decision-making.

This week, we looked at things that most investors overlook. How staking rewards aren’t just passive income—they’re behavioral training. How certain altcoins are forming the same patterns we saw last cycle, long before they moved. And how your biggest edge might just come from doing the boring research before the excitement returns.

So yeah—timing matters. But mindset matters more.

And as this cycle keeps building, that’s the one thing you can keep sharpening no matter what the candles do.

See you next week.

-A.Z.

Founder, Freedom Finance

P.S. Money moves in cycles, patience wins, and most people panic at exactly the wrong time. That’s what we cover here at Freedom Finance—real market moves, actual strategy, none of the usual nonsense.

We’re also running a $100 Portfolio as a public experiment. No magic formulas, no hype—just seeing what happens when you invest small, stay consistent, and make decisions like an actual investor. Because if you can’t manage $100, why would you handle $10,000 any better?